Clients are worried about life after retirement: Here’s how you can help

Help retirees flex their financial plans to deal with today’s challenges.

The primary benefit of a workplace retirement plan is to provide employees a path to a secure financial future, with enough money saved for a dignified retirement. And the ultimate purpose of retirement plan design is to give participants confidence in their ability to achieve their retirement goals.

For those of us in the retirement planning industry—retirement plan advisors, plan sponsors, and plan providers like Nationwide—we’ve made it simple for participants to enroll, save and invest for retirement. These innovations have helped increase plan participation and retirement preparation.

Now it’s time to take the next step – helping workers achieve financial security after they retire. Just as 401(k) and other defined contribution plans helped employees accumulate savings for the long term, we need to help participants create income from their retirement savings so they can retire with confidence, knowing they won’t outlive their income. In-plan protected income solutions can go a long way toward making this happen.

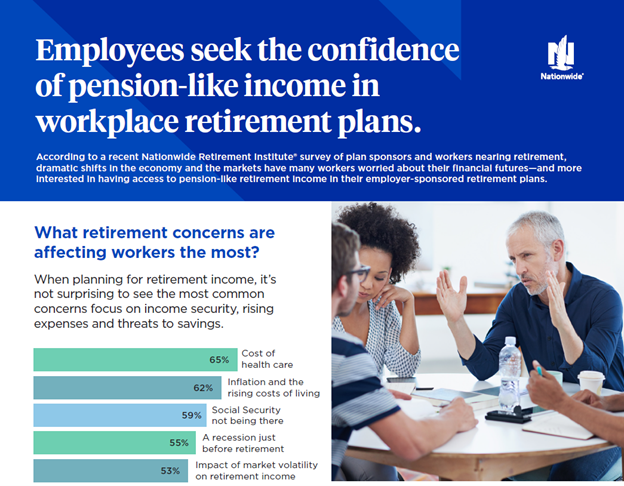

Workers are facing outside pressures from economic upheaval, inflation, and skyrocketing health care costs, and these forces are undermining their retirement confidence. A recent survey from the Nationwide Retirement Institute® found that many participants have adjusted their retirement plans over the past year, expecting to work longer and feeling less confident in their ability to be financially secure in retirement.

According to our survey, nearly one in four participants now expect to retire later than they had planned a year ago. Around 10% of participants don’t think they’ll ever be able to retire.

What can we do as retirement planning professionals to help build retirement confidence and put more employees back on track to a secure financial future? This is where protected income solutions play an important role.

One of the things we wanted to understand when conducting our survey was, why are so many employees delaying retirement? The top reasons given include fears of future recessions, the likelihood of outliving their retirement income, and the inability to afford their desired retirement lifestyle. Persistent market volatility and future market crashes were other concerns that also ranked highly.

Income insecurity and savings erosion are at the root of these fears. In-plan solutions that offer protected retirement income are specifically designed to address these risks, which is why they are proving to be popular with workers. In our survey, 87% of all participants said they’d likely rollover their current savings balance into a protected retirement income solution if one was available on their retirement plan menu.

Retirement confidence is also a concern for employers as delayed retirements can have an effect on their business operations. Our survey found employer impacts ranging from higher compensation and benefit costs, constrained ability to hire new talent, and even lower employee morale and productivity.

Plan sponsors are also seeing greater interest from employees around improving their retirement preparedness. Within the past year, 72% of plan sponsors reported greater focus from employees on retirement planning. The quality of retirement benefits may also be a factor in employee turnover, with around 40% of employers reporting an increase in workers leaving for other companies and organizations that offered better benefits over the past year.

According to our survey, protected retirement income solutions are highly rated by plan sponsors. Over 70% expressed interest and viewed them favorably and their “comfort” with protected retirement income solutions have increased year over year. However, there are some obstacles to overcome when discussing protected retirement income with plan sponsors; one-quarter of those who do not offer protected income solutions said they didn’t know enough about it and considered the solutions too complex.

Given the volatility in the economy and financial markets, a protected retirement income solution offers employees the financial security they need to feel confident in their plans for retirement.

It’s not surprising to see that many plan participants wish their 401(k) operated more like a pension according to our survey. This desire is particularly strong among participants who are getting closer to retirement; 73% of participants aged 45 or older wish their 401(k) plan offered a pension-like income stream.

Employers can play a critical role in helping their employees retire when they want by offering protected retirement income solutions as part of a world-class benefits package. Interest in these solutions is also strong among plan sponsors, with 87% wishing their plans offered pension-like income streams.

Protected retirement income solutions are built to address the very concerns that are eroding participants’ retirement confidence. This is our opportunity as retirement planning professionals to help employers bring protected retirement income solutions to their workplace retirement plans.

Learn how you can help retirement plan sponsors and participants understand the benefits of protected retirement income with solutions from Nationwide.

Retirement plan Financial Professionals: Click here

Retirement plan sponsors: Click here

Edelman Data and Intelligence (DXI) conducted a national online survey of n=600 US retirement plan sponsors and n=1,200 US retirement plan participants on behalf of Nationwide from August 10 – August 28, 2023.

As a member in good standing with The Insights Association as well as ESOMAR Edelman Data and Intelligence conducts all research in accordance with local, national and international laws as well as in line with all Market Research Standards and Guidelines.

Investing involves market risk, including possible loss of principal, and there is no guarantee that investment objectives will be achieved.

Guarantees are subject to the claims-paying ability of the issuing insurance company.

Provisions of these options may vary based on plan selection and/or by state regulation. These investment options may not be available in all states.

NFM-23301AO