Clients are worried about life after retirement: Here’s how you can help

Help retirees flex their financial plans to deal with today’s challenges.

Ten years ago, the Nationwide Retirement Institute® partnered with The Harris Poll to conduct our first survey on Americans’ knowledge and concerns about Social Security. Some things about Social Security haven’t changed much since 2014 – many people continue to rely on Social Security benefits for financial security in retirement, and many people continue to worry about whether Social Security will be there for them when they retire.

But what has changed is the greater role financial professionals play today in helping their clients make Social Security decisions, from maximizing their lifetime benefits to integrating Social Security into their overall retirement plan.

After ten years of survey results, the importance of working with a trusted financial professional to make these decisions is more apparent than ever. Financial professionals play valuable roles in providing education that builds knowledge and confidence among their clients.

Social Security confidence exceeds knowledge.

Social Security has been part of the fabric of American life for nearly 90 years. The program has changed a lot over that time, but most people still have a good handle on the basics, such as their age of eligibility.

Most US adults surveyed (89%) expressed at least some confidence in their Social Security knowledge. Surprisingly, younger generations, including millennials, were more likely to claim they’re very confident—significantly more than Gen Xers and baby boomers (25% vs 15% and 14%, respectively).

Yet, our survey also found actual knowledge about the specifics of Social Security was lacking:

What about the future of Social Security?

It’s not a stretch to say people are worried about Social Security’s uncertain future. This year’s report from the Social Security Board of Trustees (released this past March) warned that the Old Age and Survivors Insurance (OASI) Trust Fund – the federal account that pays Social Security benefits to retired workers and their surviving spouses – is expected to be depleted by 2033. That’s one year earlier than the 2022 projection. After 2033, the Board of Trustees estimates Social Security will only be able to pay 77% of benefits to program recipients unless Congress fixes Social Security.

Concerns about the future funding status of Social Security have long contributed to doubts about the program’s viability, to the point where one-quarter of those polled in this year’s survey said they don’t expect to receive a dime from Social Security. In our survey from 10 years ago, two out of three individuals aged 50+ (66%) expressed worry about Social Security running out of funding during their lifetimes. The results of our 2023 survey show these doubts have become more prevalent. Now, three out of four people aged 50+ (75%) are worried about Social Security running out of money during their lifetime.

Retirement income planning beyond Social Security.

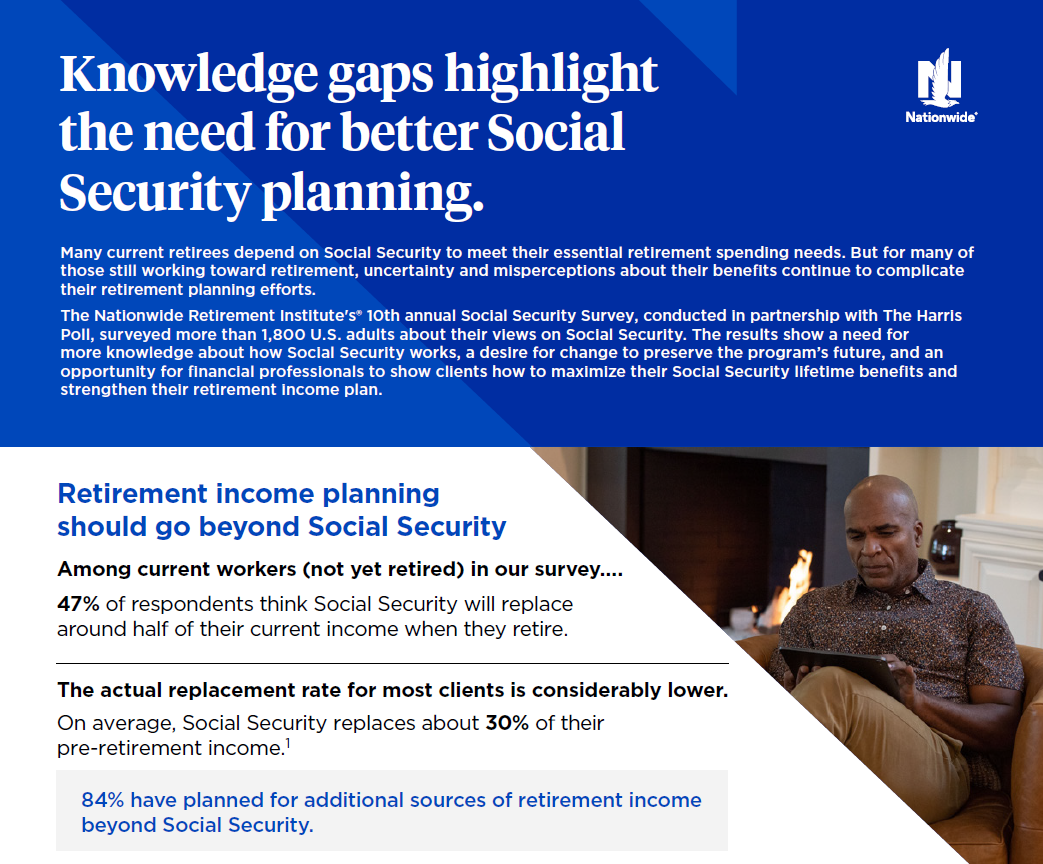

Social Security is an important component of income for a significant number of today’s retirees. Many count on these benefits to help cover their basic living expenses throughout retirement. Replacement rates for Social Security vary by income, of course, but for upper-income retirees, Social Security, on average, replaces around 30% of their pre-retirement income.1

Among future retirees, many are counting on Social Security to cover a significant share of their future living expenses. According to our survey, current non-retirees, on average, expect Social Security to pay for 47% of their retirement costs. While that estimate may be accurate for some future retirees, many in higher income brackets in retirement may be surprised by the enormous gap between their earlier expectations for Social Security and the financial reality of what their actual benefits will cover.

And yet, many people – retired and yet-to-retire – also recognize the necessity of having multiple sources of income during retirement. Over four-fifths (84%) of US adults we surveyed said they have or plan to have additional sources of retirement income besides Social Security. Most people expect to draw this income from retirement accounts or personal savings.

It’s encouraging to see that so many people recognize the need for diverse sources of retirement income. But we saw some other shortcomings in our survey around retirement income planning that should be addressed. For instance, just over half of US adults (56%) were still determining when they think their retirement savings will run out. This uncertainty was significantly higher among women than men (61% versus 51%).

Where financial professionals fit in.

Retirement income planning has quickly become a hot topic for financial professionals to discuss with clients. Ten years ago, these conversations weren’t happening often enough. In our 2014 survey, when the survey was among Americans aged 50 or older, just 29% who work with a financial professional and have not been advised about Social Security said they expect their financial professional to provide Social Security advice. In 2023, that number is much higher, at 43% among Americans aged 50 or older who work with a financial professional and have not been advised about Social Security.

Fortunately, many financial professionals have gotten the message. Around three in five American adults who work with a financial professional (62%) stated their financial professional had offered guidance on how to file for Social Security benefits. But that means two in five aren’t getting that guidance. And that gap doesn’t even include people not receiving guidance because they don’t work with a financial professional.

Many American adults who work with a financial professional or plan to ask one about Social Security (79%) said they’d switch to a new financial professional if their current partner couldn’t show them how to maximize their Social Security benefits.

Many clients would be well served by a broader discussion about Social Security planning with their financial professional. Our survey found that three-quarters of American adults want to learn how inflation could impact their retirement (78%). A similar number of American adults who plan on drawing Social Security are interested in discussing how to use different income streams to delay their Social Security filing until full retirement age (75%). And 58% are interested in understanding Social Security strategies for spouses, with a quarter of those surveyed very interested in this topic.

Resources to help your Social Security conversations.

Nationwide offers a wide range of resources on Social Security planning that you can use in your planning conversations with clients.

Your clients will benefit from understanding why maximizing Social Security is such an important part of their retirement plans. Clearing up the many misperceptions about Social Security can not only add knowledge and build confidence, but it can also help them stay on track toward their long-term retirement goals.

“Social Security Series, Part 1: The Dilemma,” United States Government Accountability Office (05/23). For the fourth income quintile with a median income of just over $81,500 per year in 2017

The research was conducted online in the U.S. by The Harris Poll on behalf of Nationwide among 1,806 adults age 18+ who currently receive or expect to receive Social Security (“national sample”), including 300 Gen Z (age 18-26), 500 Millennials (age 27-42), 504 Gen Xers (age 43-58), and 502 Boomers+ (age 59+), and oversamples for a total of 532 Hispanic adults, 507 Black adults, and 105 Asian adults. The survey was conducted May 18 – June 13, 2023.

This material is not a recommendation to buy or sell a financial product or to adopt an investment strategy. Investors should discuss their specific situation with their financial professional.

Federal income tax laws are complex and subject to change. The information is based on current interpretations of the law and is not guaranteed. Nationwide and its representatives do not give legal or tax advice. An attorney or tax advisor should be consulted for answers to specific questions.

Nationwide Investment Services Corporation (NISC), member FINRA, Columbus, Ohio. The Nationwide Retirement Institute is a division of NISC.

Nationwide, the Nationwide N and Eagle, Nationwide is on your side and Nationwide Retirement Institute are service marks of Nationwide Mutual Insurance Company. © 2023 Nationwide

NFM-23242AO