Shifts in stock market leadership can be extreme

Small caps have led the market recently, taking over from large caps. What will it take for the rally to continue?

In my weekly capital markets review, I cover the factors that have influenced market movements, share insights on stock market performance, and connect the dots on key events to watch for in the upcoming weeks.

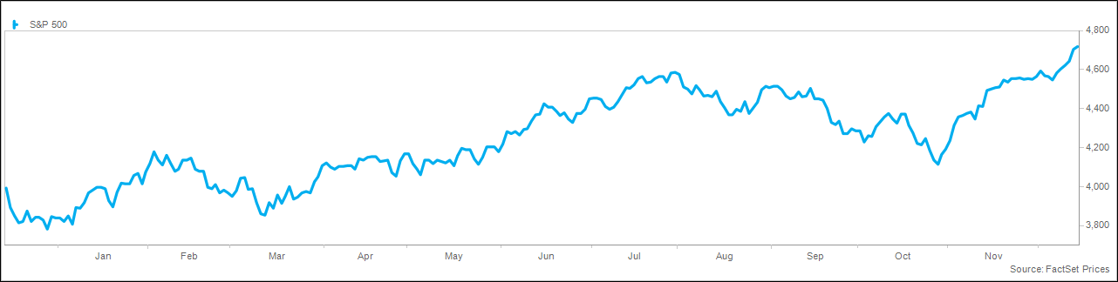

The impressive rally in risk assets continues, with the S&P 500® Index on pace for a seventh week of gains, the longest streak since 2017. The Dow Jones Industrial Average touched a record high for the first time in nearly two years. During that period, the S&P 500 gained 15% to move within 2% of a record high, now returning 24% through 12/14. The rally during that time has been broad based, with small caps gaining 22%, international stocks adding 14%, and the Bloomberg US Aggregate Bond Index returning 8%. The 10-year Treasury yield now down more than 1% over the past two months. The outlook for 2024 is cloudy due to countervailing forces. The macro “canaries in a coalmine,” notably the yield curve and leading indicators point to a recession, while the data tell a different story. Equity valuations are elevated, suggesting the market is pricing in a soft landing, though if the Magnificent 7 are excluded, valuations are reasonable.

The persistent upward pressure on equities has had a material impact on investor sentiment and positioning. Bank of America’s Bull & Bear Index jumped to the highest level since February and the largest two-week rally since 2015, aided by flows into high yield, strong credit market technicals, and improving breath in the global equity market. The Index is now neutral after being a zero on a scale from 0-10 as recently as October. Equity funds and ETFs have seen inflows in each of the past nine weeks, totaling $148 billion for the year, though that has been overwhelmed by the $1.4 trillion this year. The $5.9 trillion in money market assets could act as “dry powder” for risk assets next year as the Federal Reserve moves to cut rates, with last week being the first outflow in eight weeks. On average, the S&P 500 has rallied 19% following the Fed’s first rate cut.

The consumer is showing few signs of fatigue despite budgetary pressures and an easing job market. Retail sales jumped an unexpected 0.3% in November, better than October’s 0.2% decline and the consensus estimate for a 0.1% drop. Versus a year ago, sales rose 4.1%, with real growth of 1.0% despite the fall in gas prices impacting gas station sales. This data was reinforced by Bank of America’s Consumer Checkpoint saw card spending per household up 0.5% in November after falling on October, driven by strong real income growth across all income and age groups. Costco noted that holiday spending is ahead of expectations, with improvement in discretionary spending. The drop in interest rates has spurred optimism for consumers, with the rate on the 30-year mortgage below 7% after approaching 8% last month, driving mortgage applications up 7% in the latest week.

Wednesday’s FOMC meeting release and press conference ignited hopes for a soft landing, with a notably dovish shift by Chair Powell. The committee unanimously voted to keep rates unchanged, with Powell noting that additional hikes are unlikely unless inflation reaccelerates. The changes to the Summary of Economic Projections (so-called “dot plot”) included lower inflation for 2024 (2.4% vs. 2.6% in September), but weaker economic growth (1.4% vs. 1.5%). Notably, Chair Powell energized bulls by saying the Fed doesn’t need a recession to cut rates, driving the Fed Futures market to embed six cuts through next year (70% chance of a cut in March) versus the median of the “dot plot” at three cuts. The rally in equities may be making Fed officials uneasy, with NY Fed President Williams telling CNBC that while rates are at or near sufficiently tight levels, it is premature to talk about rate cuts. On Thursday, both the Bank of England and the European Central Bank also voted to keep policy unchanged, while both pushed back against the idea that rate cuts are imminent.

Inflation continues to moderate, with the Consumer Price Index slowing to 3.1% growth and core CPI to 4.0% from a year ago. Shelter (one-third of the calculation) and auto prices continue to be the primary headwind to moderating inflation, but recent data suggests that this will ease in coming months. This improvement was reinforced on Wednesday with a report on producer prices that was flat sequentially and up just 0.9% from a year ago. While the Fed focuses more on the core PCE deflator as an inflation gauge, these reports undoubtedly reinforced the dovish shift.

Equity markets continued their positive momentum, driven by encouraging inflation data and a dovish FOMC meeting. The S&P 500® Index, the Dow and NASDAQ each added 3%. The rally was broad based, with small caps beating large caps and value outperforming growth. Leading sectors for the week included real estate, materials, and industrials, while communication services, utilities, and health care lagged. Volatility remained muted, with the VIX closing below 13 for the fourth week, while trading volume was elevated.

Global markets were strong in reaction to the domestic rally and encouraging inflation data, with the MSCI EAFE Index up 2% and the MSCI Emerging Markets Index up 3%. Asian markets rallied on reports that China’s industrial output was the best since February 2022, driving Hong Kong up 5%, South Korea up 3%, China up 2%, and Japan up 1%. Europe was strong following the ECB and BoE meetings, with France up 2%, and the UK, Germany, and Italy up 1%. The trade-weighted dollar index fell 2% on the dovish pivot, with the index now negative for the year.

Bond yields continued their downward path this week on rapidly shifting expectations for Fed policy, with the 10-year Treasury yield falling 0.31% this week. The 2-year yield also fell 0.31% to 4.41%, maintaining the shape of the yield curve. Credit spreads continued to tighten on the increasingly optimistic outlook. Commodity prices bounced modestly this week following an extended period of weakness, with the S&P Goldman Sachs Commodity Index up 1% this week. Crude prices added 1% on macro optimism, while natural gas prices fell 4% on warm weather. Precious metals rose on falling rates, while agricultural commodities were mixed.

Investor sentiment and positioning continue to follow the direction of the equity market. The AAII Sentiment Survey showed bulls jump to 51%, while the gap between bulls and bears widened to 32%, both at the best level since April 2021. The CNN Fear & Greed Index rose to 67 on a scale from 0-100. Equity funds and ETFs attracted flows for the ninth straight week, the longest streak in two years at $26 billion. Bonds saw inflows for the tenth straight week, with inflows into investment grade and high yield offset by outflows from emerging markets, municipals, Treasuries, and TIPS. Money market funds lost $31 billion in the week.

Trading volume will begin to shrink next week given holiday vacations, increasing the chances of volatility. Economic data include housing starts on Tuesday, consumer confidence and existing home sales on Wednesday, revised GDP and leading indicators on Thursday, and the PCE deflator and personal spending and income on Friday.

Trailing Twelve Month S&P 500 Chart

This material is not a recommendation to buy or sell a financial product or to adopt an investment strategy. Investors should work with their financial professional to discuss their specific situation.

Except where otherwise indicated, the views and opinions expressed are those of Nationwide as of the date noted, are subject to change at any time and may not come to pass.

Bloomberg US Aggregate Bond Index: An unmanaged, market value-weighted index of U.S. dollar-denominated, investment-grade, fixed-rate, taxable debt issues, which includes Treasuries, government-related and corporate securities, mortgage-backed securities (agency fixed-rate and hybrid adjustable-rate mortgage pass-throughs), asset-backed securities and commercial mortgage-backed securities (agency and non-agency).

Bloomberg® and its indexes are service marks of Bloomberg Finance L.P. and its affiliates including Bloomberg Index Services Limited, the administrator of the index, and have been licensed for use for certain purposes by Nationwide. Bloomberg is not affiliated with Nationwide, and Bloomberg does not approve, endorse, review or recommend this product. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any date or information relating to this product.

MSCI EAFE® Index: An unmanaged, free float-adjusted, market capitalization-weighted index that is designed to measure the performance of large-cap and mid-cap stocks in developed markets as determined by MSCI; excludes the United States and Canada.

MSCI Emerging Markets® Index: An unmanaged, free float-adjusted, market capitalization-weighted index that is designed to measure the performance of large-cap and mid-cap stocks in emerging-country markets as determined by MSCI.

The Fund is not sponsored, endorsed, or promoted by MSCI, and MSCI bears no liability with respect to any such funds or securities or any index on which such funds or securities are based.

S&P 500® Index: An unmanaged, market capitalization-weighted index of 500 stocks of leading large-cap U.S. companies in leading industries; it gives a broad look at the U.S. equities market and those companies’ stock price performance.

S&P Indexes are trademarks of Standard & Poor’s and have been licensed for use by Nationwide Fund Advisors. The Products are not sponsored, endorsed, sold or promoted by Standard & Poor’s and Standard & Poor’s does not make any representation regarding the advisability of investing in the Product.

Nationwide Funds are distributed by Nationwide Fund Distributors LLC, member FINRA, Columbus, Ohio. Nationwide Investment Services Corporation, member FINRA, Columbus, Ohio.

Nationwide, the Nationwide N and Eagle and Nationwide is on your side are service marks of Nationwide Mutual Insurance Company. © 2023 Nationwide

NFN-1565AO