Shifts in stock market leadership can be extreme

Small caps have led the market recently, taking over from large caps. What will it take for the rally to continue?

November’s stock market rise was notable, but last month’s bond market rally may send investors a more significant (if subtle) message: the Federal Reserve has reached the end of its 20-month-long rate tightening cycle. Over the past few weeks, a series of softer economic reports and dove-ish Fedspeak from central bank officials have shifted the market’s outlook for future monetary policy, from interest rates remaining “higher for longer” to pricing in potential rate cuts as soon as next year. For example, Fed Governor Christopher Waller boosted the rate cut narrative in comments on November 28, stating he wouldn’t necessarily argue that rates remain current if inflation continues to cool. That statement gave the market its first timeline for possible rate cuts in 2024.

The recent narrative shift, however, is not the first time the bond market has signaled a Federal Reserve pivot to more accessible monetary policy. According to Deutsche Bank, market participants have priced in a Fed pivot seven times over the last two years. Still, the shift to a softer monetary policy failed to materialize each time. In assessing the latest narrative shift, investors should note that a myriad of factors can influence the direction the market takes. Market reactions to Federal Reserve rate pauses or rate cuts depend mainly on the reasoning behind the decision. Don’t take it as a given that Fed pauses or cuts will always be positive for equity markets.

First, a key issue with historical averages of past market cycles is that each cycle had its unique variables, most notably relating to what is happening in the economy. For example, during the cycle of Federal Reserve policy easing between 2001-08, rate cuts were seen as a reaction to economic weakness and risk-off market sentiment, but that wasn’t the case for the rate cuts of 1995-98.

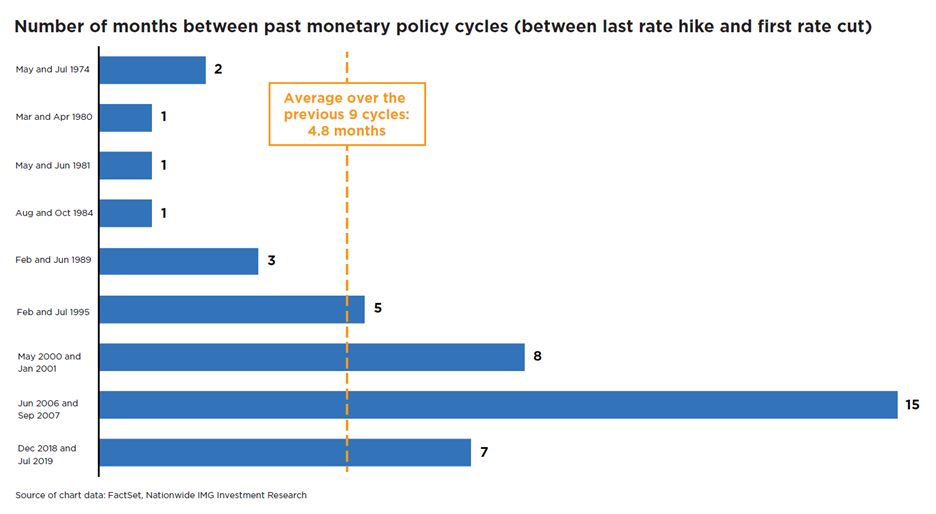

Second, assuming stocks always go up after the last Fed rate hike of the cycle, they miss the wide range of market outcomes that occurred during prior periods of Fed rate tightening. Whether the Fed decides to pause or cut, market participants should not assume that past cycles are proxies for the current cycle. For example, over the past 50 years, there have been around five months on average between the last Fed rate hike of the cycle and the first rate cut. Yet, there’s a large amount of variability between each cycle. In recent rate cycles, the Federal Reserve has frequently intervened to enact policy changes through various lending facilities. Because the central bank has lately not always used rate cuts as a blunt tool to affect economic conditions, the timing between the rate-tightened to the rate-easing cycle has extended beyond five months.

Let’s turn to the present cycle. The Fed’s last rate hike was around five months ago, so we’ve already reached the average time between cycles. If the Fed can maintain the current pause and then begin to ease rates in 2024 with an economy that is not spiraling into a recession or re-igniting inflationary pressure, stocks rally similarly to their 1995-98 performance. However, a significant divergence between Gross Domestic Product and Gross Domestic Income suggests that growth is less robust and signals a potentially ominous omen for the economy. Further, if the economy weakens in 2024 and the Fed starts to cut rates in response to the drop in growth, like what occurred in 2001-08, this backdrop usually does not bode well for equities.

Investors should avoid extrapolating equity market performance based on past cycles. A better approach is to monitor economic data in the coming months to see if the data confirms the bond market’s exuberance for easing rate expectations.

This material is not a recommendation to buy or sell a financial product or to adopt an investment strategy. Investors should work with their financial professional to discuss their specific situation.

Except where otherwise indicated, the views and opinions expressed are those of Nationwide as of the date noted, are subject to change at any time and may not come to pass.

Nationwide Funds are distributed by Nationwide Fund Distributors LLC, member FINRA, Columbus, Ohio. Nationwide Investment Services Corporation, member FINRA, Columbus, Ohio.

Nationwide, the Nationwide N and Eagle and Nationwide is on your side are service marks of Nationwide Mutual Insurance Company. © 2023 Nationwide

NFN-1555AO