6 tips to enhance client communication for financial professionals

Robust client communication skills can set you apart from your counterparts, leading to improved client satisfaction, retention, and referrals for your practice.

Key Takeaways:

For Hispanic Heritage Month (Sept. 15 – Oct. 15), we’re turning the spotlight on the second-largest demographic and fast-growing segment of the U.S. population. In 2020, Hispanic Americans comprised nearly 19% of the overall population, a tremendous rise over the last 50 years.1 Hispanic Americans control an increasing share of personal wealth through investment and business ownership.

While Hispanic Americans share many of the same financial goals and concerns as all Americans, there are some key distinctions that financial professionals can focus on to help their Hispanic clients build greater financial confidence and security.

Recently, Nationwide conducted a survey of U.S. consumers, including a significant population of Hispanic adults, to understand more about the distinctions that influence differences in financial decisions.2 You can learn about these distinctions in our recent infographic.

Hispanic adults are feeling the squeeze of inflation, much like the general U.S. population. Nearly nine in 10 Hispanic adults said they are concerned about current levels of inflation in the country. That includes over 60% of Hispanic adults who are very concerned about inflation.

Inflationary pressures are contributing to a negative perception of the U.S. economy among Hispanic adults; 56% of those surveyed said the economy is getting worse, which is mostly in line with the overall U.S. population.

The impact of inflation on Hispanic adults is changing some financial behaviors, including 46% who said they have dined out less often in the last 12 months because of inflation. Moreover, 35% of Hispanic adults reported higher prices have led them to drive less, seeking to pay less at the gas pump.

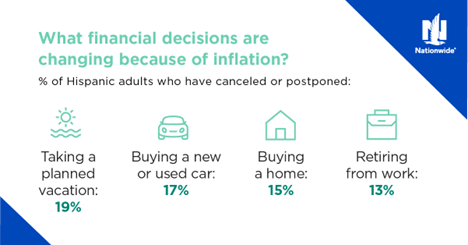

These immediate changes would be expected in a time of rising prices and are largely consistent with the general population. However, when it comes to larger purchases or longer-term financial plans, many Hispanic adults are doing things differently. For example:

Looking more closely at decisions about retirement, the differences between Hispanic adults and the overall U.S. population become starker. Older Hispanic adults (those in the Boomer and Gen X age groups) were more likely to have put off retirement recently than the same age cohorts in the general population. This is also true of Hispanic adults with more than $100,000 in investable assets, so wealth doesn’t seem to factor much in the decision to delay retirement.

However, there is one factor that does seem to make a difference – working with a financial professional (FP). Hispanic adults who are working with FPs were less likely to have postponed retirement than those who are not.

It’s not just inflation that’s affecting Hispanic adults as they make these major financial decisions. The rise in market volatility this year is also taking a toll on their financial outlooks. There’s also the ongoing impact of COVID-19, which continues to compound the financial challenges faced by Hispanic Americans.

Let’s address COVID first, which in many ways has continued to influence Hispanic Americans more than the general population. In our recent survey, 57% of Hispanic adults said they are re-evaluating their financial plans due to the financial impacts of COVID-19. For the general U.S. population, this share is just under half, at 47%.1

The pandemic is also influencing the decision on when to file for Social Security. One-third of Hispanic adults said they are doing something different with Social Security filing or are planning to. That includes 17% of Hispanic adults who said they plan to delay filing for benefits due to COVID-19, versus 11% of the overall population. At the same time, the same percentage of Hispanic adults (17%) have filed for Social Security earlier than planned or expect to do so.

Concerns about market volatility are also widespread among Hispanic Americans, where more than seven in ten (73%) said they are worried more now about the impact on their retirement income, compared with 66% of the general population.

Our survey revealed that nearly two in five Hispanic adults (39%) are currently working with a financial professional. That, of course, is good news. However, it’s younger Hispanic adults from the Millennial generation who are more likely to be already working with an FP (51%). For those in the Boomer and Gen X generations, a working relationship with a financial professional is less common – 36% of Hispanic Gen Xers and 29% of Hispanic Boomers.

But the financial challenges of inflation, market volatility and COVID across all generations of Hispanic adults can create opportunities for financial professionals to connect with them and offer guidance. Our survey found that 30% of Hispanic adults would turn to a financial professional to learn more about the impact of inflation on planning for Social Security benefits. A similar percentage (31%) said they’d talk to an FP about managing inflation and higher costs during retirement.

Perhaps the biggest opportunity with Hispanic clients is in helping them maximize their Social Security benefits using the rules around delayed filing and spousal benefits. A full 72% would be open to talking with a financial professional about managing different income streams so they could delay and potentially maximize their Social Security benefits. Another 67% want to learn more from an FP about managing spousal benefits.

From your standpoint as a financial professional, these are opportunities to connect and build relationships with Hispanic clients by focusing on their specific needs for financial education and guidance. With Social Security in particular, we’re ready to support you with tools and resources to help you extend your knowledge and start conversations with Hispanic clients.

Here are different ways Nationwide can help you address your clients’ Social Security concerns:

https://www.pewresearch.org/science/2022/06/14/a-brief-statistical-portrait-of-u-s-hispanics/, Published June 14, 2022.

“2022 Consumer Social Security Survey: Hispanic Report” Nationwide and The Harris Poll. June 29, 2022.

Survey methodology: This survey was conducted online within the U.S. by The Harris Poll on behalf of Nationwide between April 19 and May 7, 2021 among 1,853 U.S. adults age 26+ (national sample) including 674 Millennials (age 26-41), 576 Gen Xers (age 42-57), and 603 Boomers+ (age 58+) and an oversample for a total of 502 Hispanic adults, a total of 591 Asian adults, a total of 593 Rural adults. Data were statistically weighted as needed to bring them in line with the population of U.S. residents age 26+ from the 2022 Current Population Survey for age by gender, education, race/ethnicity, region, household income, marital status, and household size. To ensure the national sample was representative, the data were initially weighted by generation (Millennials 26-41, Gen Xers 42-57, and Boomers+ 58+) and then combined into a total 26+ group. Data for Hispanic, Asian, and Rural adults were weighted as needed for age by gender, education, region, household income, marital status, and household size. Our weighting algorithm also included a propensity score which allows us to adjust for attitudinal and behavioral differences between those who are online versus those who are not, those who join online panels versus those who do not, and those who responded to this survey versus those who did not.

NFM-22386AO.1