Clients are worried about life after retirement: Here’s how you can help

Help retirees flex their financial plans to deal with today’s challenges.

In the current economic climate of high inflation and interest rates, more Americans find themselves struggling with increased financial stress. That could mean different things to different people, such as families trying to make ends meet or young workers feeling the financial weight of a heavy debt burden.

As the financial stresses of today impact the outlook for the future, many Americans are coming to terms with the idea that their retirement may look significantly different from the type of retirement their parents and grandparents enjoyed.

The Nationwide Retirement Institute® polled 2,300 investors and over 500 advisors in our ninth annual Advisor Authority survey to discover how today’s economic climate is affecting their financial plans for tomorrow. Over six in ten investors (61%) in our survey said their expectations for retirement have changed significantly in the last five years.

A lot of this shift has to do with the challenges people presently face in managing their finances today, from spending, to balancing their household budgets, to paying off debt.

What’s different about today’s retirement outlook? First, many investors (61%) don’t feel the norm of retiring at age 65 as applying to them. There’s a positive aspect to this shift; many current and future retirees see the importance of staying physically and socially active, so they’re defying the idea of retirement as a time of rest.

But there’s a downside, too. Many older workers expect to keep working past age 65 because they believe they’ll need the income or need to save more for retirement. Unfortunately, while some older workers want to stay employed out of choice, a greater number find they are forced into retirement because of a layoff, a health problem or the need to provide care to a family member.

Second, many investors (50%) don’t have a “magic number” or specific target amount of retirement savings they’re aiming for. This idea was popular many years ago; think of Lee Eisenberg’s book The Number, which was first published in 2006. According to our Advisor Authority survey, today, just 38% of investors have a retirement “magic number”.

The “number” has fallen victim to shifting expectations for retirement, as well as the unpredictable nature of planning in an uncertain economic climate. Rather than to focus on a number—which is dependent on different variables such as spending habits, debt levels, area of residence and more—investors should think more about their overall financial plan and how it aligns to their long-term goals. That, more than aiming for a target, will do more to help ensure a comfortable retirement.

Economic challenges are compelling people to make some difficult financial decisions as they try to manage different financial priorities.

For instance, many people know it’s important to save for retirement, but putting money aside for the future can be hard to do when they’re dealing with so many financial challenges today. Inflation remains persistently high, especially for many essential goods and services. Plus, it looks like interest rates could stay higher for longer, which adds to the costs of many people who are carrying high levels of debt.

The squeeze is forcing many to make the difficult but important choice to forgo discretionary spending in order to keep their household budgets in balance or to avoid going into debt. This is especially true for those who are closest to retirement.

Non-retired investors age 55+ and retired investors told us they’re adjusting priorities to meet financial commitments in today’s economic environment by cutting back on many “nice to have” purchases perhaps because they’re worried about how they’ll pay their monthly bills in retirement. Some of the common discretionary purchases on the decline include luxury goods (47%), leisure activities (44%), entertainment (44%) and vacations or travel (38%).

Given this concerning outlook for Americans’ financial future, many financial professionals are stepping up to respond, “How can we help?”

Financial professionals are on the front lines of the current retirement challenge. Of those surveyed, nearly half (48%) said the rising cost of living has influenced their clients to rethink or redefine their retirement planning strategies.

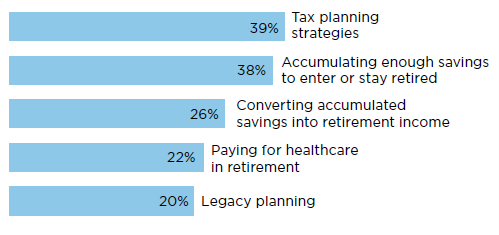

Financial professionals offer a vital support line to investors who are struggling with planning for retirement while keeping their financial house in order. Clients who are currently working with financial professionals are finding success in getting the help they need, most frequently in these areas:

What about the changing views of retirement? Nearly half of financial professionals surveyed (47%) say working in retirement is one strategy their clients are using that is considered radically different from that of their parents or grandparents. Those radical expectations often require financial professionals to think differently about the investment solutions they bring to the planning discussion. According to our survey, non-correlated assets, alternative investments and protected solutions such as annuities are all common ways financial professionals use to help protect their clients from market risk. These solutions can help solve specific challenges such as securing income in retirement and managing market volatility.

It’s clear from our surveys that having a trusted financial professional makes a difference for individual investors when it comes to feeling confident about living comfortably in retirement. Financial professionals can seize the opportunity in the uncertain economic climate to engage with clients and reinforce the importance of sticking to their long-term plan.

Resources and solutions from a trusted provider like Nationwide can help you build the trust you need to deepen your client relationships and help them meet the challenges of preparing for a secure financial future.

Investing involves market risk, including possible loss of principal. No investment strategy or program can guarantee a profit or avoid loss.

Methodology: The research was conducted online within the U.S. by The Harris Poll on behalf of Nationwide from January 8-23, 2024, among 518 advisors and financial professionals and 2,346 investors ages 18+ with investable assets (IA) of $10K+. Advisors and financial professionals included 257 RIAs, 178 broker-dealers, 130 wirehouse and 42 other financial professionals. Among the investors, there were 601 Mass Affluent (IA of $100K-$499K), 518 Emerging High Net Worth (IA of $500K-$999K), 410 High Net Worth (IA of $1M-$4.99M) and 217 Ultra High Net Worth (IA of $5M+), as well as 600 investors with $10K to less than $100K investable assets (“Less affluent”). Investors included a subset of 391 “pre-retirees” age 55-65 who are not retired.

NFM-23884AO